Only time tells what can stand the test of time

Contents

- Lindy’s Law as a Survival Heuristic

- Buffett’s Moat and Lindy’s Filter

- Monetary Assets as Coordination Technologies

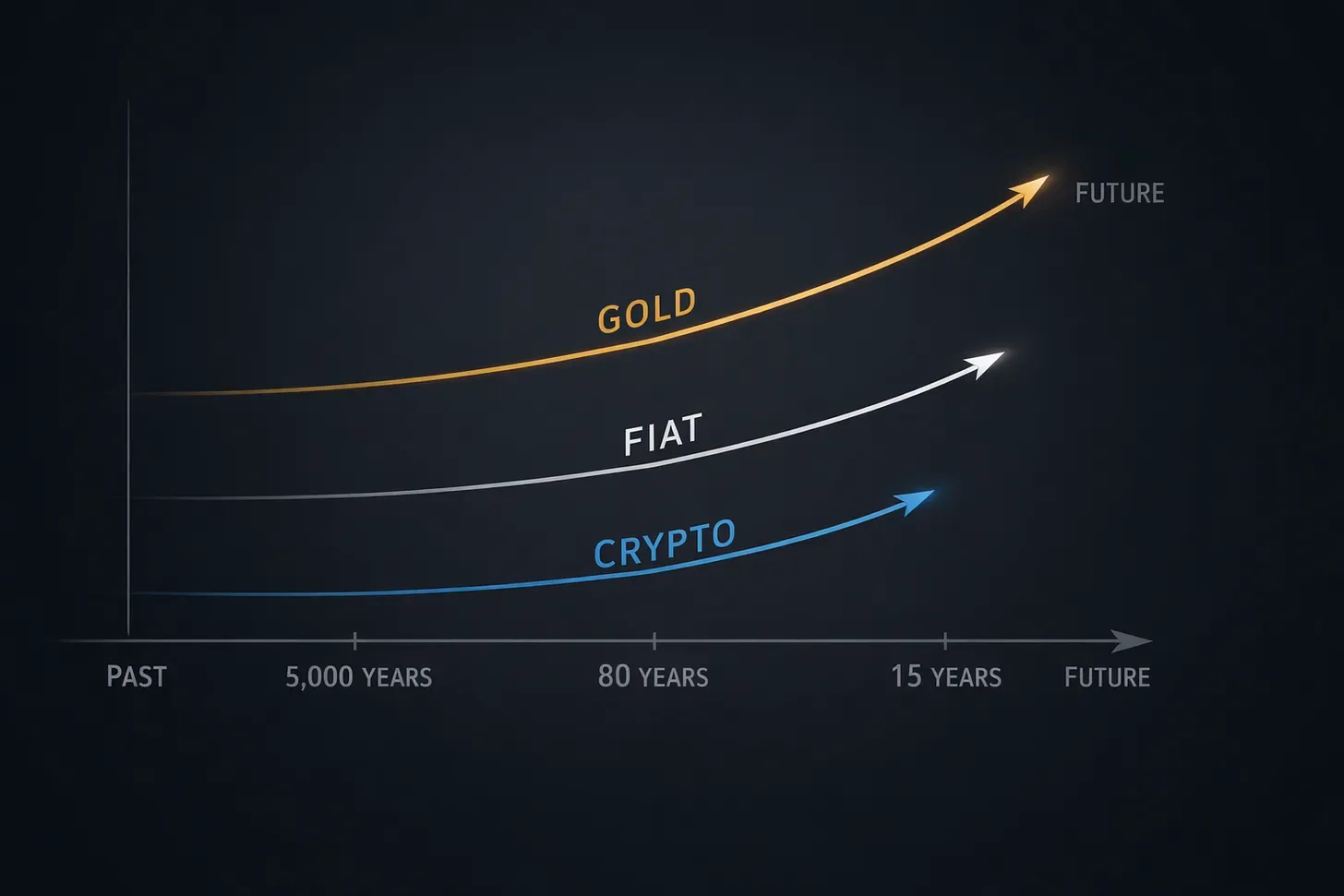

- Gold and the Lindy Curve

- Fiat’s Shorter Lindy Tail—

- Crypto and Engineered Durability

- Tether’s Portfolio Signal

Lindy’s Law as a Survival Heuristic

Lindy’s Law is not an investment framework in the conventional sense. It does not forecast returns, optimize portfolios, or estimate forward earnings. It is a survival heuristic. It is empirical rather than philosophical or theoretical. In its simplest form, Lindy’s Law observes that for certain non-perishable things such as technologies, institutions, and monetary goods, their expected remaining lifespan increases with the time they have already survived.

Put differently, if something has existed for X years, it may reasonably be expected to exist for another X years. The future life expectancy of the asset or system scales with its current age.

Buffett’s Moat and Lindy’s Filter

When placed next to Warren Buffett’s concept of a protective moat, the overlap becomes obvious.

Buffett looked for businesses that can defend themselves against time, competition, and changing conditions. Lindy’s Law looked at things that have already done exactly that. They approach the same problem from different directions:

• Buffett asks: What will still be here decades from now?

• Lindy observes: What has already proven it can be?

Buffett’s moat is prospective. It is forward looking. It evaluates whether a firm’s cost structure, brand equity, network effects, or switching costs can resist erosion over time. Lindy’s Law is retrospective. It does not speculate about whether something can endure. It measures whether something already has.

Monetary Assets as Coordination Technologies

This distinction becomes particularly useful when discussing stores of value.

Money, at its core, is a coordination technology across time. A store of value only works if economic actors believe it will preserve purchasing power into an uncertain future. That belief is not granted once and permanently. It is earned repeatedly through performance under stress. War, inflation, fiscal expansion, technological disruption, political turnover. Each of these events constitutes a challenge to monetary trust.

An asset that survives multiple such regime shifts accumulates institutional memory. Legal scaffolding builds around it. Cultural reflexes develop in its favor. Settlement infrastructure evolves to accommodate it. Over time, the system becomes path dependent. The longer it survives, the harder it becomes to replace.

Gold and the Lindy Curve

This is where Lindy intersects with gold.

Gold has functioned as a monetary asset across empires, continents, and technological epochs for thousands of years. It persisted through bimetallic standards, colonial paper regimes, the Bretton Woods system, and the post-1971 transition to fiat currencies. Each transition introduced new monetary technologies that were more efficient in transactional terms. Yet when confidence in those newer systems degraded, gold repeatedly re-emerged as the reserve layer beneath them.

Under Lindy’s Law, this longevity carries probabilistic weight. If gold has served as a store of value for millennia, then its expected remaining lifespan extends accordingly. If it has lived for 5,000 years, one may reasonably assume that it could live for another 5,000. That is not a guarantee of performance. It is an inference about survivability.

Fiat’s Shorter Lindy Tail

Fiat currencies present a different profile.

As much as policymakers might prefer a national currency to endure indefinitely, historical evidence suggests that fiat regimes rarely survive the full arc of fiscal expansion, demographic stress, and political turnover. Their adaptive flexibility allows for monetary expansion, redenomination, or replacement in response to economic crises. That flexibility enhances their usefulness as mediums of exchange and policy tools. However, it shortens their Lindy tail as stores of value.

If a given fiat currency has existed for 75 years, Lindy suggests that its expected remaining lifespan as a trusted store of value may also be on the order of decades rather than centuries. This is not to say that it will fail. It is to acknowledge that only time will tell if you can stand the test of time.

Crypto and Engineered Durability

Crypto assets face a similar challenge from a different direction.

Protocols such as Bitcoin attempt to engineer monetary durability through fixed issuance schedules and decentralized consensus mechanisms. These features are designed to resist dilution and political interference. In Buffett’s language, they constitute an attempt to build a moat through code.

Lindy’s Law, however, does not evaluate design intent. It evaluates demonstrated endurance. Crypto’s monetary history is measured in years rather than centuries. Its long-term survivability as a store of value remains contingent upon future stress tests that have yet to occur at scale. Again, this does not imply failure. It implies uncertainty that only time can resolve.

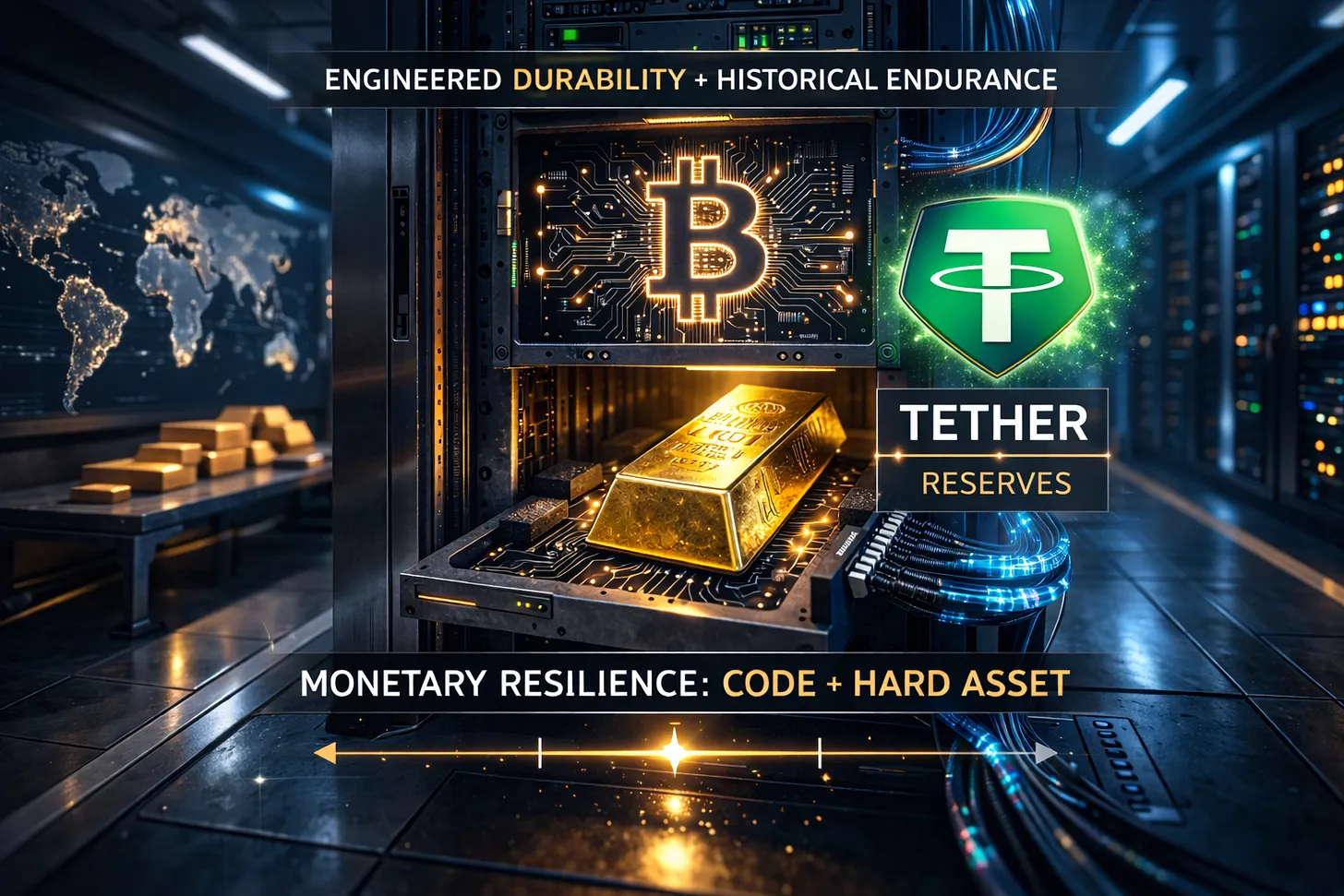

Tether’s Portfolio Signal

Which brings us to Tether.

Tether has historically positioned itself as a staunch advocate of Bitcoin and the broader digital asset ecosystem. Its reserves and investment strategies have reflected a belief in the long-term viability of decentralized monetary technologies. Yet over the past two years, the company has also begun allocating capital toward physical gold.

This shift invites a question.

Might there be any clue as to why gold is a necessary part of their own portfolio?

Public commentary from Tether’s leadership provides some context. In recent interviews, CEO Paolo Ardoino has described the firm’s evolving strategy as oriented toward building systems capable of surviving economic breakdowns and governance failures.

“We are building an ecosystem of investments that can survive a future breakdown.”

He has also emphasized that the firm’s capital deployment across infrastructure layers is intended to maintain operational continuity under conditions of institutional stress.

“We are preparing for scenarios where parts of the traditional financial system may stop working.”

That framing aligns closely with Lindy logic.

Rather than relying solely on prospective design features such as algorithmic issuance rules, Tether appears to be diversifying into assets that have already demonstrated endurance across multiple monetary regimes. Gold’s inclusion within their reserves can be interpreted as an acknowledgment that survivability in extreme scenarios may require exposure to assets with long Lindy tails.

In this sense, Tether’s gold purchases are not a repudiation of Bitcoin. They are a recognition that monetary resilience may be enhanced by incorporating assets whose historical persistence has been empirically validated.

Gold does not need to be engineered to survive future regime stress. It has already done so.

Under Lindy’s Law, that history carries forward into expectation.