Backwardation Tells the story

TL;DR

• China’s silver market remains physically tight despite stabilization in international prices, with record backwardation and decade-low exchange inventories signaling preference for immediate delivery.

• Investment bar demand and solar manufacturing procurement continue draining stockpiles, while short sellers pay deferral fees to avoid delivery, reinforcing evidence of localized scarcity.

• Speculative positioning has cooled ahead of Lunar New Year, yet structural supply constraints persist, leaving Shanghai spreads historically elevated.

• In our view, the tightening in China coincides with a broader hemispheric realignment of silver concentrate flows toward U.S. refining and banking channels, suggesting that geopolitical supply restructuring may be amplifying physical stress in Asian markets.

China’s Silver Tightness Deepens as Global Prices Stabilize

International silver prices have steadied following a period of extreme volatility, yet physical conditions inside China continue to reflect pronounced strain. Investment demand and industrial consumption are drawing down exchange inventories, tightening prompt supply and distorting futures spreads.

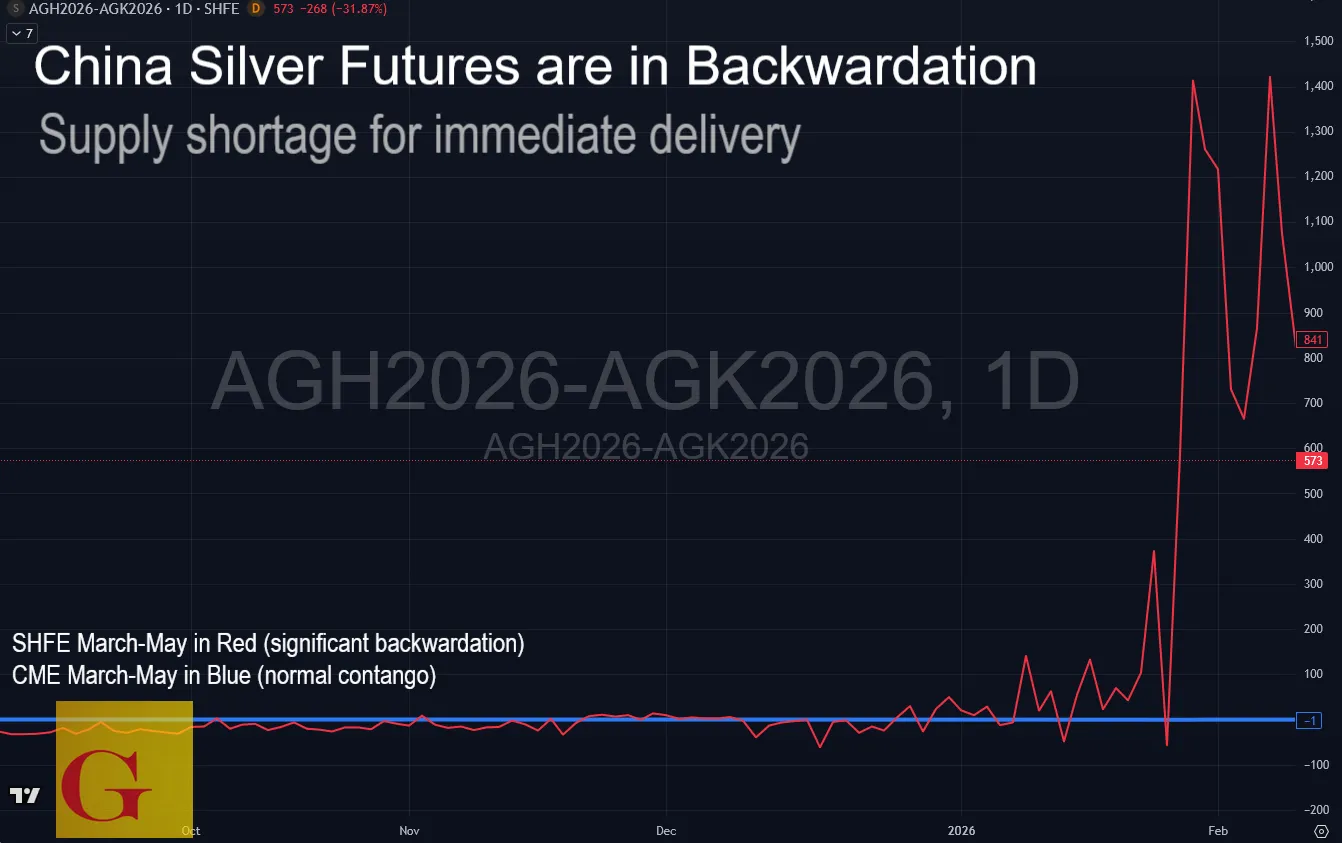

According to a February 10 Bloomberg News report, inventories across Chinese exchanges have fallen to multi-year lows while front-month contracts trade at record premiums to deferred months. The imbalance reflects a preference for immediate delivery and underscores the scarcity of deliverable material within the domestic market.

Physical Tightness Expressed Through Backwardation

Domestic producers and traders are working through backlogs of orders as near-term prices rise relative to forward contracts. The front-month silver contract on the Shanghai Futures Exchange has climbed to a record premium over the next active month. The structure signals backwardation, a condition in which prompt metal commands a higher price than future delivery.

“Such a large backwardation is driven by an inventory crisis and the depletion of deliverable material,” said Zhang Ting, senior analyst at Sichuan Tianfu Bank Co.

“Institutions still have incentives to continue squeezing the market for profit.”

The spread between the front-month and next contract has widened to levels rarely seen in Shanghai trading. Positive spreads confirm a market paying up for immediacy.

Short sellers on the Shanghai Gold Exchange have also paid deferral fees to avoid physical delivery since late December. The payments indicate limited availability of metal to settle obligations, reinforcing evidence of tightness within exchange-linked warehouses.

From Speculative Surge to Inventory Drain

The silver market experienced a historic selloff beginning at the end of January, erasing most of the 61 percent rally registered in the opening weeks of the year. That earlier advance was fueled by heavy speculative participation in China and overseas, with silver temporarily drawing flows typically directed toward gold during periods of macro uncertainty tied to the dollar, Federal Reserve governance concerns, and geopolitical tensions.

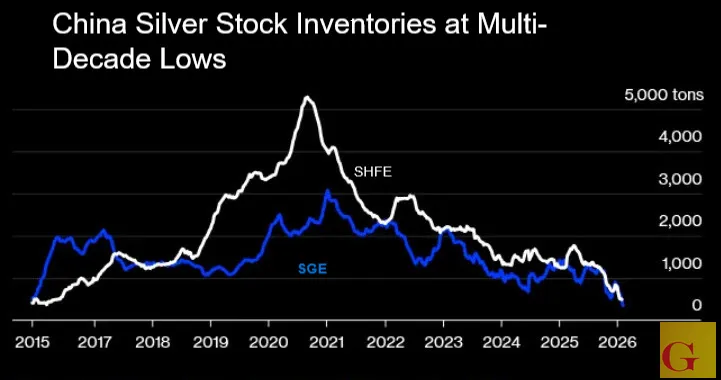

Despite the price correction, physical stockpiles remain depleted. Chinese inventories had already been reduced following an autumn squeeze on global supplies. The December surge in investment demand accelerated the drawdown.

Warehouse stocks linked to the Shanghai Futures Exchange and Shanghai Gold Exchange now sit at levels last observed more than a decade ago.

Retail and Industrial Demand Remain Firm

Investment bar demand has remained elevated. In Shenzhen’s Shuibei district, the country’s primary bullion trading hub, merchants continue to transact at premium prices.

“Whenever there are stocks, they’re sold off quickly,” said Liu Shunmin, head of risk at Shenzhen Guoxing Precious Metals Co.

Industrial consumption adds a second layer of demand. China’s solar panel manufacturers, which use silver paste in photovoltaic cells, are increasing production ahead of the April 1 expiration of export tax rebates. Some firms used the recent price decline to secure material at lower levels, according to market participants.

The convergence of investment accumulation and manufacturing procurement limits the metal available for exchange delivery.

Seasonal Constraints and Cooling Speculation

Market participants note that the only potential relief in the immediate term would come from increased smelter output during the Lunar New Year period. Historically, industrial activity slows during the week-long holiday, making a production surge less likely.

There are indications that speculative positioning is moderating. Aggregate open interest on the Shanghai Futures Exchange has declined to the lowest level in more than four years as traders reduce exposure ahead of the February 16 holiday start.

Broader Commodity Context

Separate commentary from Bloomberg Intelligence highlighted an expected acceleration in fundraising by Chinese miners amid an ongoing metals supercycle. Aluminum’s price behavior has shifted toward closer alignment with copper, reflecting substitution dynamics and shared macro drivers. U.S. officials also continue to monitor China’s crude stockpiling strategy, which may influence oil prices even during periods of global oversupply.

Within that broader commodity landscape, silver in China remains defined by localized scarcity and structural tightness. Futures spreads, warehouse levels, and deferral payments together indicate a market prioritizing physical immediacy over forward exposure.

Hemispheric Supply Realignment and Strategic Silver Flows

The tightening visible inside China coincides with a broader restructuring of global silver sourcing, particularly across Latin America. Over the past several months, U.S. policy and private-sector initiatives have increasingly redirected concentrate flows toward domestic refining capacity, reshaping traditional supply pathways that previously fed Asian processing centers.

This development aligns with what GoldFix has described as a modernized hemispheric resource doctrine: a renewed emphasis on securing critical mineral supply chains within the Western Hemisphere. The practical expression of that posture has been the expansion of U.S. refining initiatives and greater reported intake of silver concentrate sourced from Latin American producers.

The political shift in Venezuela, including the removal of Nicolás Maduro from power, accelerated reassessment of regional resource flows. Venezuela, while not a dominant global silver producer, sits within a broader geopolitical corridor influencing mining and trade relationships throughout South America. Policy recalibration in Caracas has been interpreted in markets as part of a wider consolidation of Western-aligned supply channels.

At the same time, industry reporting has indicated increased receipt of silver concentrate within the United States by major financial institutions and affiliated refiners. Banks such as JPMorgan, already central to global precious metals warehousing and futures infrastructure, are understood to be expanding their interaction with physical flows of concentrate destined for domestic processing. While granular positioning data remains opaque, concentrate imports and refining throughput suggest a strengthening Western accumulation channel.

This hemispheric realignment intersects directly with the physical tightness documented in China. If Latin American concentrate that might otherwise have been refined for Asian delivery is increasingly routed through U.S. facilities, available supply into Chinese exchanges becomes structurally constrained. In such an environment, backwardation in Shanghai reflects both local inventory depletion and the friction introduced by altered trade routes.

The convergence of exchange backwardation in China and strategic intake in the United States presents a two-pole structure in the global silver market. One center exhibits immediate delivery stress and decade-low warehouse stocks. The other center expands refining capacity and concentrate absorption within a national security framework tied to critical minerals policy.

In this configuration, silver transitions from a purely cyclical industrial metal to a strategically managed asset embedded within competing supply architectures. The inventory crisis in Shanghai therefore exists alongside a deliberate redirection of hemispheric flows, reinforcing the broader structural narrative that physical metals are increasingly shaped by geopolitical design as well as market forces.