Change is here and it is not going away

The revolution is in use, not in gold itself. In Stage One, which we are still in, you must own gold. In Stage Two, which will come relatively soon, you must use your gold as collateral to harness its buying power

TL;DR — Follow the Gold Flow Monster

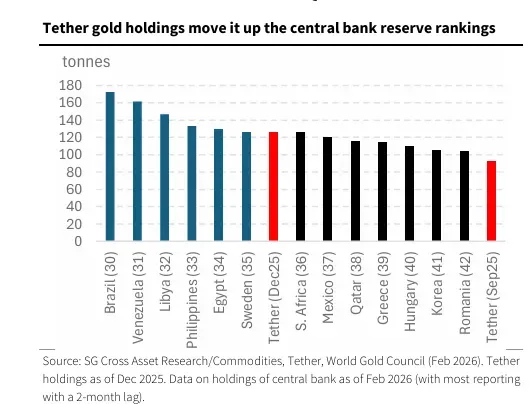

- Tether is now a measurable force in physical gold demand, holding 125 (now About 148) tonnes by Q4 2025. That places it alongside central banks and within the top 10 global gold “fund” holders by size.

- Its quarterly inflows rival sovereign buyers and major ETFs, and daily modeled flow data suggests it is increasingly relevant to short-term price dynamics, especially during futures-driven volatility.

- Gold is gaining payment rails. Tokenized, 1:1 backed gold transforms bullion from static reserve asset into digitally transferable collateral embedded in blockchain infrastructure.

- Our view: Stage One is accumulation. Stage Two is monetization. As gold integrates into collateral frameworks and digital settlement systems, those who already own it stand to benefit from expanded utility, liquidity, and systemic relevance.

The Emergence of a New Gold Actor

The first four pages of Société Générale’s Commodity Compass (see at bottom1) introduce what the authors describe as a structural shift in gold market flow analysis: the rise of Tether Gold as a measurable and increasingly dominant force in physical gold demand.

The report frames the development directly:

“One component of the gold market that is rapidly growing in influence is Tether.”

This is not presented as a marginal phenomenon. Rather, the bank argues that Tether’s audited Q4 2025 gold holdings and persistent inflows now demand the same analytical attention historically reserved for ETFs, central banks, and hedge funds.

By December 2025, Tether’s accumulated gold holdings reached 125 tonnes. The report observes that if ranked alongside sovereign institutions, this would position Tether as the 36th-largest “central bank” holder globally. Within ETF comparisons, it would rank 8th out of 388 tracked vehicles by tonnage. In quarterly inflows, it would have ranked second behind SPDR in Q4.

The analytical implication is straightforward: digital gold issuance is no longer peripheral to physical market structure.

The Stablecoin That Took the Central Bank Path

The authors emphasize that Tether Gold operates on a 1:1 basis with physical bullion meeting LBMA Good Delivery standards. In structural terms, this aligns it closely with physically backed ETFs, even though it exists within the digital-asset ecosystem.

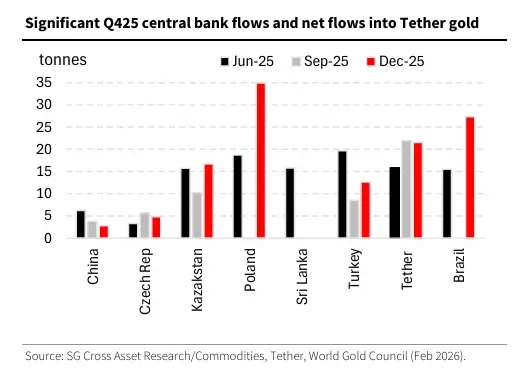

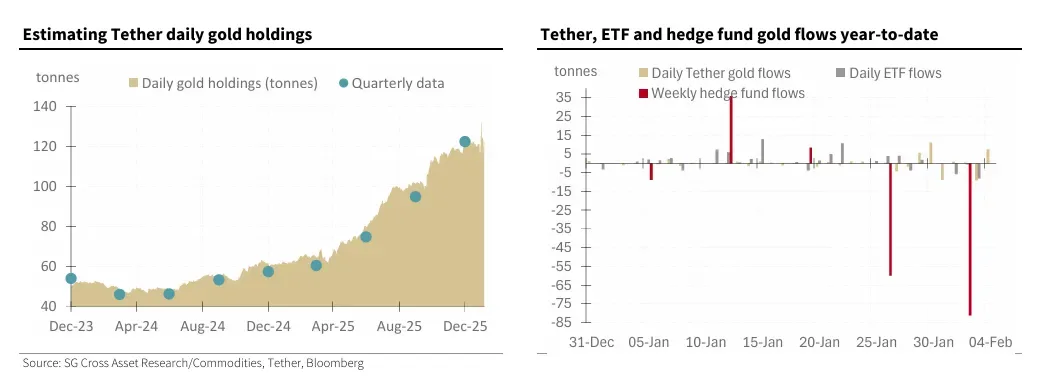

Holdings were stable between 48 and 52 tonnes from Q2 2023 through Q3 2024. The acceleration begins thereafter. In Q2 2025, holdings rose by 15.8 tonnes. In Q3 and Q4 2025, an additional 22 tonnes were added each quarter.

The report highlights the scale of that accumulation:

“Only two central banks accumulated more gold than Tether: Poland… and Brazil.”

In other words, within the official-sector league table of quarterly buyers, a private digital-asset issuer placed third.

This reframes the gold market from a sovereign-dominated narrative toward a hybrid model where digitally intermediated physical ownership contributes meaningfully to aggregate flows.

ETF Comparisons and Market Hierarchy

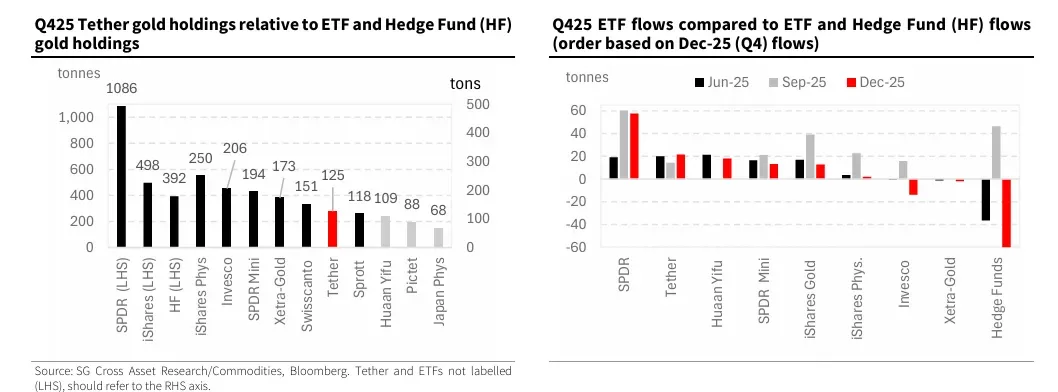

Total global ETF holdings stood at 4,144 tonnes as of January 30, 2026. SPDR Gold Shares alone held 1,089 tonnes; iShares held 498 tonnes.

Against that backdrop, Tether’s 125 tonnes appear modest in absolute scale. Yet ranking 8th globally in tonnage, without being legally structured as an ETF, underscores the speed of digital gold adoption.

More significant than static holdings are marginal flows. In Q4 2025, Tether’s inflows would have ranked second among all ETFs, surpassed only by SPDR.

This shifts the marginal-buyer framework. If ETF flows have historically served as a proxy for Western institutional demand, Tether flows may increasingly represent digitally native or globally distributed demand pools.

Hedge Funds and the Price Discovery Layer

The report then situates Tether within the broader architecture of gold price formation. Hedge funds, via futures and options, remain a dominant force in price discovery. Converted to tonnage equivalent, hedge funds held approximately 392 tonnes at the end of Q4.

This would rank them as the third-largest ETF-equivalent holder if treated as a single entity.

However, quarterly hedge-fund outflows in Q4 amounted to roughly 60 tonnes, nearly matching SPDR inflows and exceeding Tether’s quarterly additions.

The authors stress the distinction:

“Hedge fund gold flows, although ‘paper trades,’ can have a significant impact on price discovery in both futures and physical markets.”

Position limits constrain any single hedge fund’s physical equivalent exposure, but aggregate positioning shifts remain large enough to generate substantial price volatility.

The key analytical question becomes whether Tether acts as a countercyclical physical stabilizer during futures-driven volatility.

The Data Lag Problem and the Daily Flow Solution

A structural limitation in gold-flow analysis has always been timing asymmetry. Central bank data are reported with lag; CFTC positioning arrives weekly; ETF flows are daily. Tether quarterly reserve disclosures also arrive with delay.

The innovation described in the report addresses this constraint directly:

“We can complement these with an estimated daily flow series for Tether.”

The methodology is mechanical and balance-sheet based. Starting with quarter-end reserve composition, daily market returns are applied to model expected reserve values. The divergence between modeled reserves and observed token market capitalization reflects net token issuance. Assuming proportional reserve allocation, daily gold purchases can be inferred in ounces and converted to tonnes.

The result is a real-time estimate of Tether’s physical gold accumulation.

January Case Study: Buying the Dip

From late December through mid-January, ETF and hedge-fund flows dominated price influence. In the final week of January, however, Tether’s flows became comparatively dominant relative to ETFs.

After a sharp price decline on January 30, Tether reportedly added approximately 11 metric tonnes, effectively absorbing some of the downside pressure.

The authors conclude succinctly:

“Tether’s influence on the gold market now cannot be ignored.”

This is the central thesis. The digital issuance of tokenized gold has crossed from marginal innovation into systemic flow factor.

For gold analysts accustomed to monitoring COMEX positioning and ETF tonnage tables, a third pillar now exists: algorithmically inferred crypto-physical flows operating in near real time. The gold market’s structure is increasingly hybrid, integrating sovereign accumulation, institutional ETF demand, speculative futures positioning, and digitally intermediated physical ownership.

GoldFix: Gold Gets Payment Rails

SG states that Tether’s influence cannot be ignored. That conclusion extends beyond quarterly flow comparisons. It signals a structural shift in how gold is used inside the financial system.

Tether reflects a transformation in gold’s monetary plumbing similar to what the BRiCS are doing on their end to monetize Gold for public and international use in trade. A token backed 1:1 by allocated bars turns bullion into a digitally transferable financial instrument embedded in blockchain infrastructure.

This changes velocity. Gold can move across digital rails with settlement characteristics closer to stablecoins than vault transfers. Accessibility expands. Transferability becomes continuous. Gold integrates directly into digital balance sheets. Gold Goes Public!

Ownership patterns will evolve. Sovereign vaults, ETFs, and private custody remain foundational. Yet blockchain-based gold introduces a parallel channel that broadens participation and deepens liquidity. It puts Gold on its own payment rails

This development does not alter what a sovereign individual should do with physical metal. Direct custody retains its structural role in wealth preservation and independence. That foundation stands.

However, wider digital monetization increases the utility and financial relevance of the asset class. As tokenized gold scales, physical holders benefit from a larger demand base, greater liquidity, and deeper integration into financial architecture.

The revolution is in use, not in gold itself.

Tether is an early signal. Blockchain infrastructure is reshaping how gold functions as collateral, settlement asset, and balance sheet component. That shift is underway and warrants attention.

In Stage One, which we are still in, you must own gold. In Stage Two, which will come relatively soon, you must use your gold as collateral to harness its buying power to grow your economy, personal or otherwise.